Life seems to be having a bit of a retro 1970’s moment. On one hand we have tensions in the Gulf spilling over into an oil crisis of sorts (the depth of which is very much dependent on where in the world you are located), meantime NASA is flying to the moon again. The past month has seen the US indices shake off the former and latch on to the latter to spur on a gravity defying market ascent.

As we concluded in our commentary last month Wall Street was ripe for a relief rally and the markets certainly ripped. At time of writing as the month draws to a close the S&P 500 was up more than 10% for April and the Nasdaq in truly stellar fashion put in more than 15% (if you’ll pardon the astronomical pun).

Seeking Reasons

So what interpretation should be placed on this trampoline like turn around? The conflict in the Gulf remains very far from resolved. This was illustrated by Brent hitting its highest level thus far since the conflict began as it momentarily crossed $126/barrel in the dying hours of April.

Some would put this down to a yet again exceptionally robust US economy, everything from healthy consumer spending to the return to favor for the AI stocks. Others would caution that wars and their economic consequences do not get wished away and cannot be easily brushed under the carpet, even when they are several thousand miles away.

Convincing arguments can be found to explain and justify either stance depending on the position one takes. This debate even comes down to the cost of war itself. The Department of War revealed a spend of $25B so far on the Iran war, with the bulk of that spent on munitions. For some, the replenishing of these weapons stocks represents future government subsidized job support for those in the relevant defense sectors for years to come. For others this is treasure needlessly wasted on a war of choice.

Remaining Alert to the Dangers of Assumption

In a way the sudden recovery following a sudden decline, has become so synonymous with US market activity that it has almost become assumed that it will and even that it should happen. As though it reflected some, necessary, natural economic equilibrium. Inverse gravitation if you will – what goes down must come up. This is a dangerous and false assumption.

The sobering highlight from the final Fed statement with Jerome Powell as head was as obvious as it was direct:

Developments in the Middle East are contributing to a high level of uncertainty about the economic outlook.

You would be hard pressed to find any agreement with that statement among the happy market participants who spent April soaring to the moon. However those in the Federal reserve appear to live in a different dimension than that of the market trader. A place where time moves at a different pace due to the reality of economic lag.

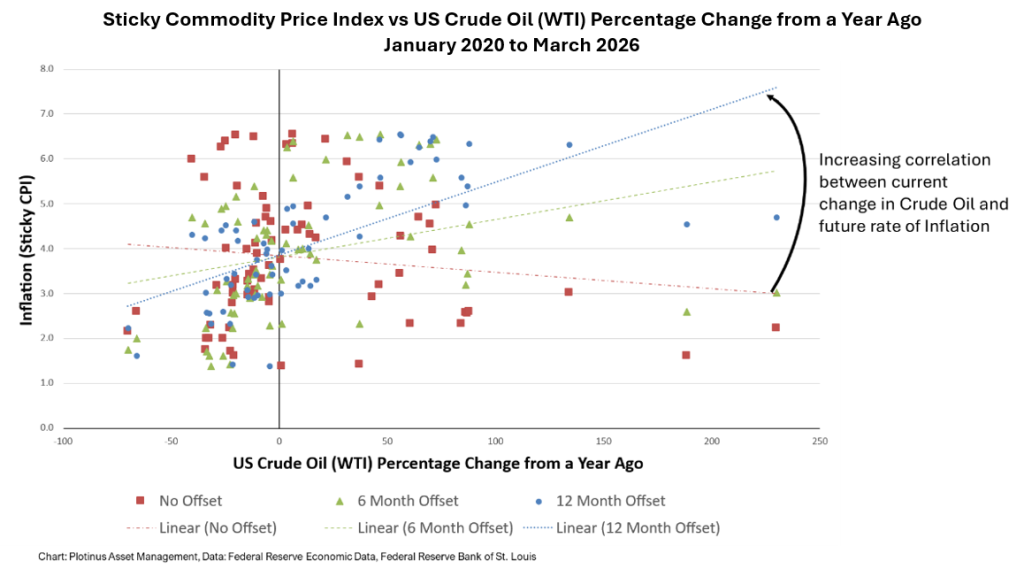

We will conclude with a simple chart that should provide some food for thought as to where that line in the Fed statement is coming from. It illustrates the relationship between the yearly percentage change in US WTI crude oil and the Sticky CPI inflation measure.

This is interesting because of course the Sticky CPI excludes direct fuel inflation. Therefore we are seeing the indirect effects of the fluctuations in the price of oil on inflation. The chart looks at the relationship between previous changes in oil and inflation 6 months hence and 12 months hence. It provides an indication for the potential inflationary implications of the war with Iran. ■

© 2026 Plotinus Asset Management. All rights reserved.

Unauthorized use and/or duplication of any material on this site without written permission is prohibited.

Image Credit: NASA.