In the last month the DJIA and NASDAQ have both entered into a market correction (a 10% fall) from their previous high and the S&P has been skirting with correction territory losing around 9%. Corrections are a regular part of market dynamics, however, given the ongoing war in the Middle East, the question is whether this current correction can be viewed in any sense as being normal?

The year began with much discussion of the lopsidedness of the growth of the US markets, where 2025’s gains were overwhelmingly fueled by the AI boom with the inevitable discussion of when the party might begin to end. Prior to the beginning of operation Epic Fury the NASDAQ as the focal point of the AI/Tech world was already negative YTD down -2.5%, having peaked on 28 January. This was very much in line with the AI/Tech cooling narrative. The more broad based Dow Jones was portraying its less Tech concentration, with YTD up +1.9% whilst similarly being down from it peak reached on 10 February.

The last four weeks have illustrated that if the year began in some kind of normative framework of understanding—it certainly is not there now.

The Dynamics of Uncertainty

Both the DJIA and NASDAQ have fallen in tandem, from 27 February (the day before the conflict began) up to 30 March. The DJIA fell -7% and the NASDAQ -8% respectively. This degree of correlated drop, in our opinion, reflects the market response to the war and its dynamics of uncertainty, and not the prior cyclical market dynamics.

What should be of most concern to investors is that this war response, may well be in addition to those dynamics that could have manufactured a correction due to investment in AI/Tech cooling off. Not that the war is acting as a catalyst for them. In other words, the pre-war cool off is yet to properly manifest. Put this in the context of the economic consequences so far, higher oil, aluminum, fertilizer, petrochemical prices, the abandonment of any expectation of Fed rate reductions, the looming specter of increased inflation, the outlook for US markets remains deeply uncertain.

In light of this uncertainty it is tempting to seek comparisons for the market impacts due to geopolitical instability. As we discussed in our commentary last month, this can potentially be deeply flawed, requiring us to find a new framework in which to analyze the current circumstance. Take for instance the war in Ukraine. It would seem to be logical to find parallels. A contemporaneous regional conflict with the potential to spiral into a broader theatre. A conflict with a very direct and immediate impact on world oil and gas supply. However, beyond very broad brush stroke comparisons it doesn’t provide very substantive material to help with present market analysis of what is in essence a very, very different war.

Trying even to look at the basic impact on oil, is not very useful. In the first month of the Ukraine War, WTI increased by 22% and Brent Crude by 23%. In the first month of the Iran War, WTI has increased by 53.5% and Brent Crude by 55.6%. It should be noted that the actual dollar price of oil (not adjusted for inflation) by the end of March 2022 was still higher than it is today.

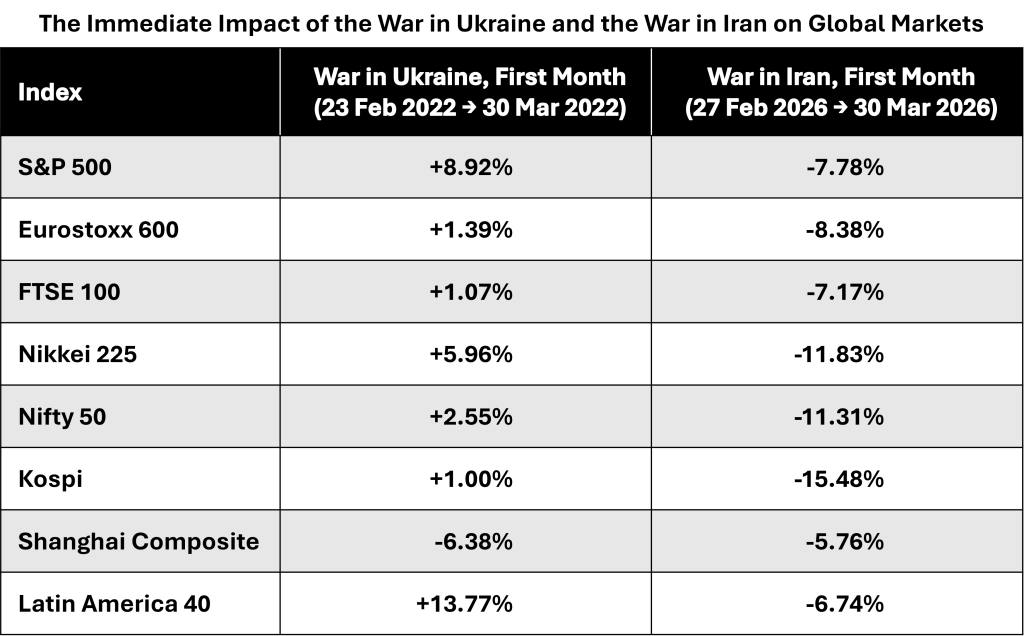

Look also at the following table, tracking the effect (or lack thereof) on various world stock indices a month into each of the two wars.

Of course it is too simplistic to completely equate these stock market returns, particularly the losses directly with the War in Iran but the picture of the globally negative results this past month cannot be ignored. There is no doubt that the current war is of deep concern in every corner of the world. The same cannot be said for the War in Ukraine, which, in spite of Volodymyr Zelenskyy’s valiant efforts to keep it to the forefront of world politics, has increasingly, as time has gone by, been viewed as a European regional conflict.

Rearing for a Rally

The US market does have the potential to be buoyed, perhaps momentarily in the event that the administration suddenly announces, “War is Over”, even unilaterally and even at the expense of appearing weakened, by as has been suggested, abandoning the Strait of Hormuz in a state of Iranian closure. The US markets have been excessively sensitive in buying into supposed good news when there is very little meaningful content to back it up, as Wall Street is ripe for a relief rally and maybe the problems will just go away.

The problem is that, regardless of whether this war ends in the morning or not. Considerable global economic damage has been caused by the injection of a splurge of uncertainty.

In the event though that this war does continue for the foreseeable future, several more weeks or months. The reality of commodity dislocation is going to manifest itself painfully throughout the world. The combination of heightened oil prices and the rupture in normal supply is not something that will be easily resolved without causing severe economic damage, particularly in emerging markets. US stock markets in the long run are not so disconnected from the rest of the world as not to be damaged if they are unable to bounce with the US into a Truth Social-based recovery. ■

© 2026 Plotinus Asset Management. All rights reserved.

Unauthorized use and/or duplication of any material on this site without written permission is prohibited.

Image Credit: Invent-mkp.