The UK celebrated the 10th anniversary of Brexit by fittingly dumping yet another Prime Minister. Keir Starmer’s coup de grace resignation allowed him to avoid being thrown to the wolves by his own party in a leadership challenge.

In the post Brexit era, Starmer should be proud. His few remaining weeks in power before his replacement is enthroned, means he will manage to serve out an average term length of 2 years. To put this in some context David Cameron the last pre-Brexit politician served 6 years 63 days and before that Tony Blair and Margaret Thatcher clocked in over a decade in power each.

The investor question of course is does this pronounced shift from political stability to instability have any economic/investing relevance?

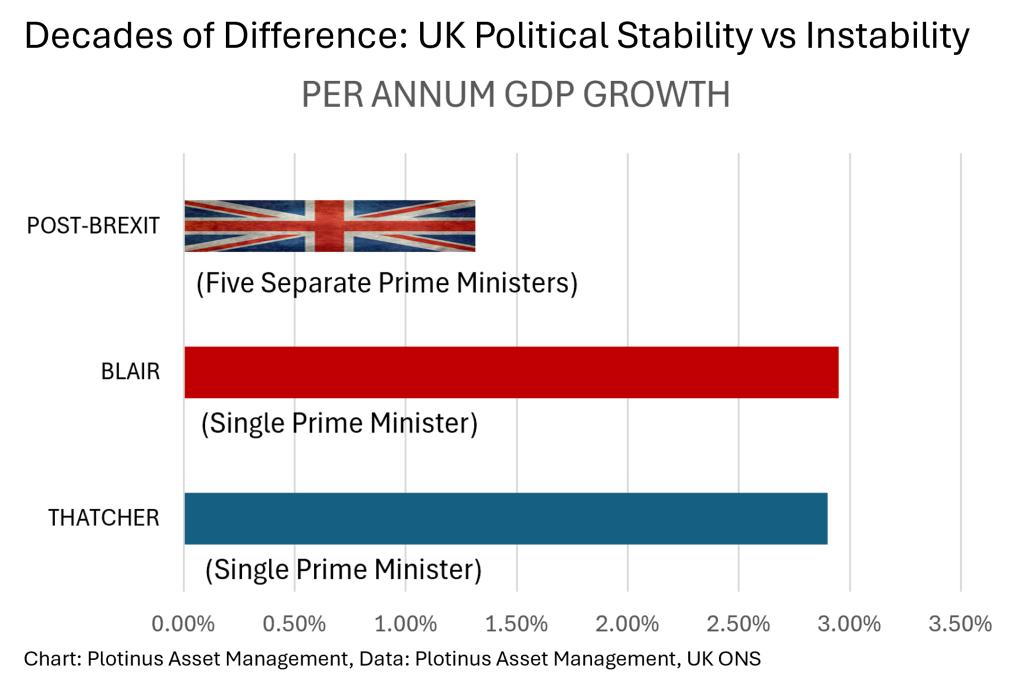

The simple answer is yes. The post-Brexit decade has had an average UK GDP growth of 1.3% per annum, Tony Blair’s term averaged 2.9% and Margaret Thatcher hit a similar 2.9%. Cumulatively that makes quite an impact. Britain ended up being more than 20% better off after a decade of stability rather than one with prime ministerial musical chairs.

Regno Unito?

Italy was once the classic text book case for political instability, crumbling governments and a merry-go-round of changing prime ministers. This though has somewhat changed. The Italian Prime Minister has lasted just 1.80 years on average since Margaret Thatcher became British Prime Minister in 1979. However in the past decade Italian Prime Ministers have lasted 2.38 years which is longer than their British counterparts.

A Broader Picture

It is too simplistic to conclude that the UK’s relative political instability has caused a drop in annual GDP growth. The interconnecting realities behind the GDP figures are much more complex, woven into the larger world macro-economic fabric

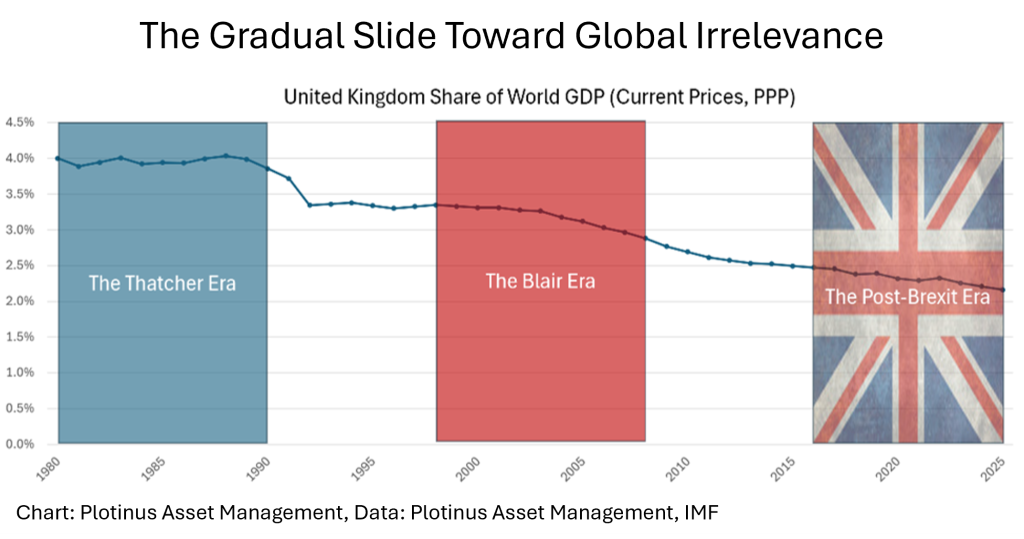

The following chart illustrates the UK’s declining share the of World GDP—in effect this represents its economic/political clout on the world stage. As can be seen, that relevance has almost halved since the time of Margaret Thatcher, as the share of World GDP has fallen from 4.00% in 1980 to 2.16% in 2025. Note that the base measure used to calculate this share is GDP, current prices (Purchasing Power Parity), we consider in this instance to be the measure that best reflects the actual relative wealth of Britain vs the world.

Essentially this means that Britains experience themselves as being almost 50% poorer than they did in 1980. In this light the political instability is not surprising and can be seen as being symptomatic of a greater malaise, somewhat reflecting the general loss of direction, relative poverty, and diminishing stature on the world stage.

Interestingly one of the criticisms of Keir Starmer has been that he has been too focused on international issues and not sufficiently focused on fixing domestic problems. Mr Starmer’s assumed replacement Andy Burnham’s agenda, seems to be very domestically focused. Whilst decentralizing from a London-centric nation and regional levelling up may be crowd pleasing rhetoric, the only way to rectify the UK’s deep-seated problems is through the creation of a vibrant, dynamic economy. That must be driven by an outward looking nation, both attractive for inward foreign investment and an exporting powerhouse.

Is it G7, G1(6) or maybe G2(3)?

The annual G7 meeting in Evian (France) a few weeks ago, highlighted the same kind of issue of dwarfing global relevance that can be seen affecting Britain. The G7 structure now looks like a dusty antiquated format. It no longer feels like a meeting of equals working toward collective geopolitical and economic approaches. Instead it looks like the US and six lesser parties a G1(6) instead of a G7. The choreography of the latest event in Evian belied this reality.

On the other hand though, the EU being given a seat at the table, rectifies this economic imbalance presented by the US vs everyone else. In fact it could be argued that a G2(3) two equal parties US and EU and three lesser parties (Japan, UK and Canada) might be a more constructive and meaningful format. In reality though this cannot happen as the EU is not just the sum of its parts, and remains much less powerful and unified than its sum might suggest.

It is ironic that the moves to attempt to create a more powerful unified EU are the very things that ignited the push for Brexit, fuelled by a resentment of the threatened loss of sovereignty. Ten years on, it is estimated that the UK economy is 6%-to-8% smaller than it might have been had the UK remained in the EU. “Going it alone” has shown itself for what it was—a reductionist viewpoint with the result being a comparable economic weakening and reduction in influence on the international stage. In the same period of time the EU too, has stumbled by not establishing itself as a global superpower. In its half-baked state, it has been humiliated by Russia, a weak adversary, and also by the US (its supposed ally).

Mr. Burnham the expected new occupant of Number 10 Downing Street has an opportunity to “Go Big,” visionary, opening a (difficult) pathway reasserting Britain in the heart of a more assertive, powerful Europe or to “Go Home.” The information to hand presently indicates that it will likely be the latter choice and Manchester it will be. If so, this choice for smallness will be to the further long-term detriment of the UK. ■

© 2026 Plotinus Asset Management. All rights reserved.

Unauthorized use and/or duplication of any material on this site without written permission is prohibited.

Image Credit: GB-funkyart-images.